Pictures can be worth a thousand words! As we close the book of 2021, we thought our readers might find it interesting to reflect on some of the most remarkable developments of the year, illustrated graphically. Commodity prices, currencies, equity markets, interest rates, inflation: these are the topics that we discuss in this special edition of our investment letter, highlighting where and why our expectations were borne out and – even more importantly – what might lie ahead for 2022.

1. Booming energy-related commodity prices

Oil proved one of the best performers of 2021, up nearly 60%, and with it other energy-related commodities. Coal for instance closed the year just under USD 140 per ton, double where it was trading in early January, and having hit a record USD 269.50 at the beginning of October.

To us, this rally in energy prices came as no surprise. In fact, we think that the oil price could again defy consensus expectations in 2022. This because of the combination of still strong demand and constrained supply. On the demand side, not only has the post-pandemic recovery not yet run its course, but, on a more medium-term term horizon, the energy transition will actually – somewhat paradoxically – be supportive. As we pointed out last June, the route being taken to reach carbon neutrality by 2050 (e.g. improving building isolation) often makes heavy use of petrochemical products. This, even as activists and financiers are dissuading energy companies from investing in new exploration projects, OPEC+ is only very gradually expanding its quotas (out of decision but also sheer capacity) and US shale producers – the marginal actor on the supply side – remain very disciplined.

2. Euro down against most major currencies

As the graph makes clear, the euro lost ground in 2021 against most major currencies, Japanese yen excepted. We attribute its weakness to a combination of relative central bank stance (the European Central Bank remains much more accommodative than the Federal Reserve, Bank of England or Norges Bank notably) and relative economic growth (with European GDP only now recouping its 2019 level, whereas Switzerland and the US did so already mid-2021).

We also depict the Turkish lira’s (bad) performance in 2021, as an example of what a non-democratically led country can experience. Their currency’s loss in value has been such that private sector employees in the main cities of Turkey are now asking to be paid in hard dollars.

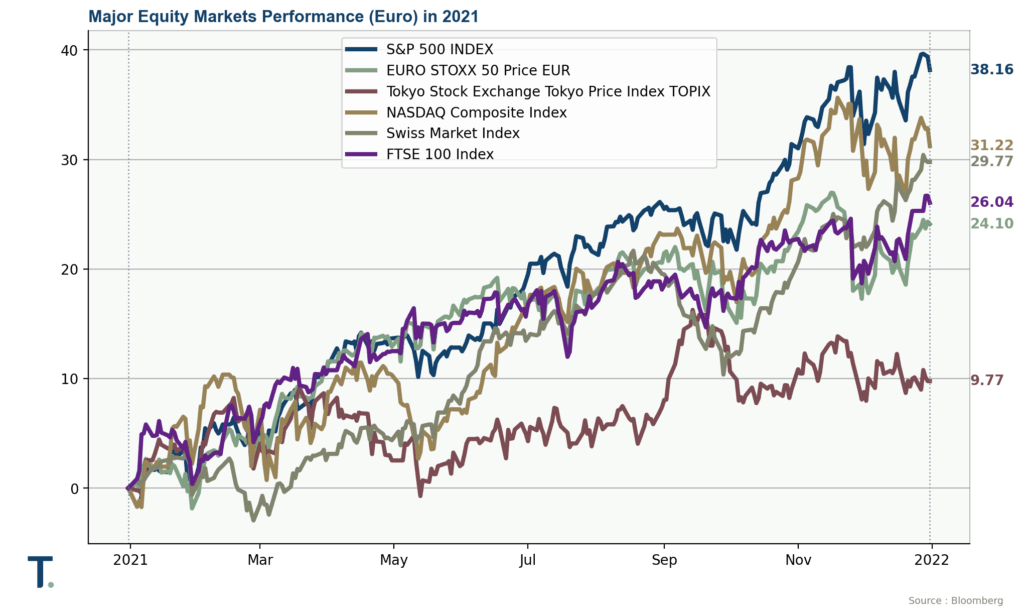

3. Equity markets: THE place to be

Outside of China, equity markets enjoyed a stunning 2021, in local currency terms and even more so (because of the aforementioned currency trends) in EUR. This, as we repeatedly mentioned during the year, has to do with the TINA (“there is no alternative”) factor. Real rates are negative, meaning that fixed income instruments do not protect against a loss of purchasing power due to inflation. Also, when the US and European central banks eventually do hike rates, bonds will drop in value. Equity markets thus retain our and other investors’ favour, despite valuations that can only be described as rich.

But, as also mentioned repeatedly in recent months, we recommend limiting equity risk through diversification and a focus on companies that have pricing power or are well positioned to benefit from the emerging wave of energy transition-related investments. And we believe that derivative portfolio protections are ever more warranted going into 2022.

As for Chinese equities, their underperformance (indeed negative return in local currency terms) stems from the 2021 interventionism of the country’s authorities, particularly in the high-tech sector. And, of course, the troubles in the Chinese real estate sector, epitomised by Evergrande.

4. 10-year yields still near historical lows

The long-term government bond rates chart is the mirror image of that depicting major equity markets. Indeed, it is precisely because safe fixed income instruments yield hardly any return that investors flocked into stocks during 2021 – and will likely continue to do so in 2022.

That said, rates are not moving freely. It is central bank interventions that are keeping yields so low despite the – not so transitory as we discuss below – inflation flare. Simply put, the level of government debt across the globe has become such (courtesy of the pandemic but not only) that rising rates would render its financing increasingly difficult.

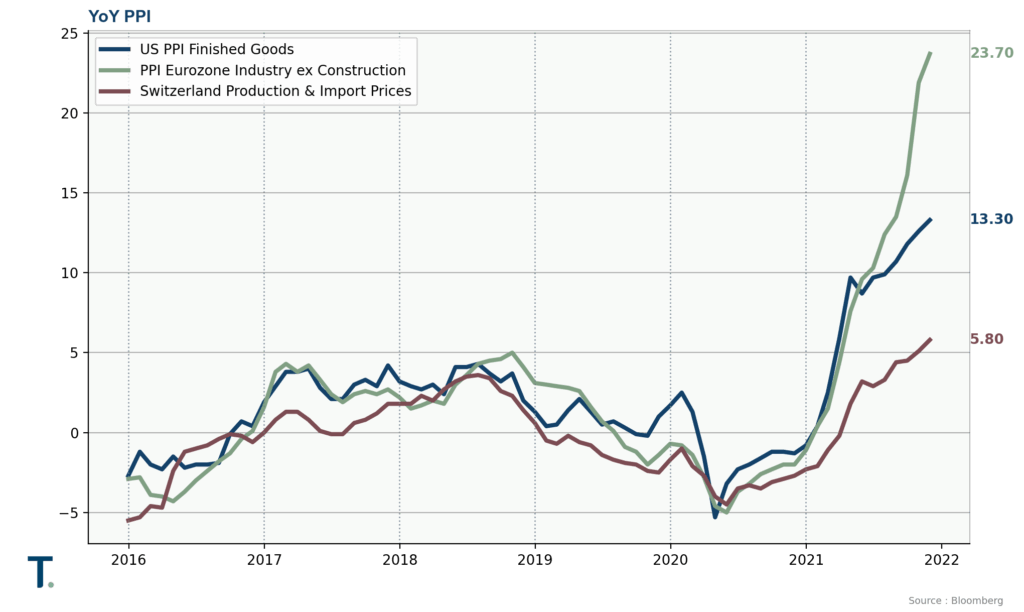

5. Consumer and producer price indices at levels not seen in decades

Our first investment letter of 2021 began with these words of warning: “Topping our list of what could go differently – not to say wrong – would of course be issues pertaining to vaccine deployment but also a spike in inflation.” Well, price indices certainly did flare up in 2021, recently approaching 7% in the US on the consumer side (producer price inflation being much higher even) and 5% in Europe. As much as central banks hoped that these pressures would be only transitory, they have now had to acknowledge this might not be the case and thus moved forward their intended tapering.

One of the key issues for 2022 will be whether a wage-price spiral sets in, which would effectively anchor inflation into the system…

Best wishes to our readers and their families for the New Year!