Just when the major financial actors had lowered and postponed their rate cut expectations, better aligning them with Federal Reserve and European Central Bank projections, the Swiss National Bank surprised everyone by cutting its policy rate by 0.25% on 21 March. The low level of domestic inflation effectively gave it the luxury of being the first among major Western central banks to pivot monetary policy – with the strong Swiss franc and concerns about economic weakness in the EU, the country’s largest trading partner, obviously also playing a part. While investors understandably cheered the news, they should nonetheless be wary not to let stock prices get ahead of themselves.

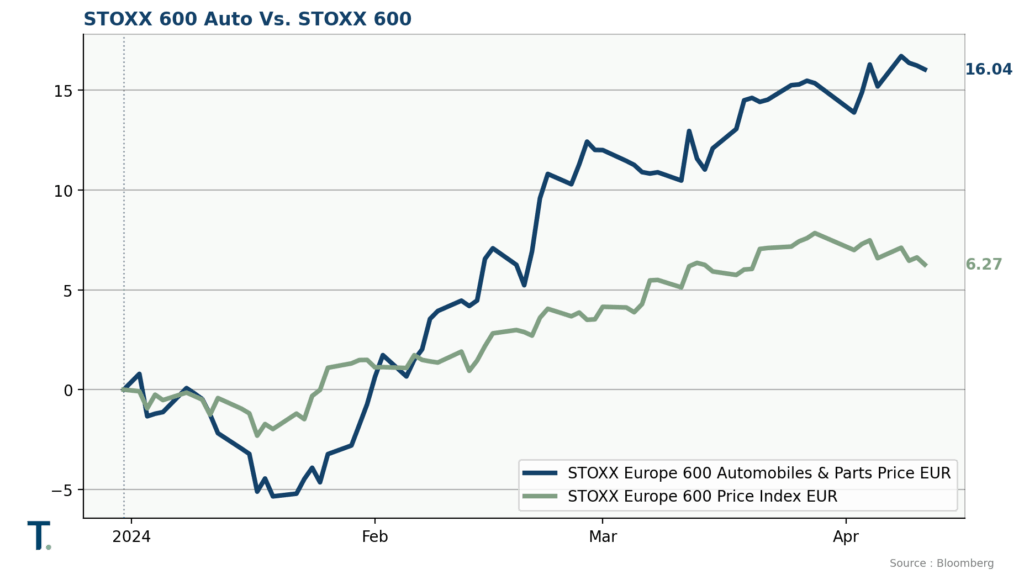

Among the strongest performers of the past few weeks figure, curiously, some European car makers, both in the luxury segment (e.g. Mercedes) or at the middle- to lower-end of the market (e.g. Stellantis, born of the merger of the Peugeot and Fiat groups). Beyond the fact that their valuations had become very cheap, investor interest in such names seems to stem from their “best of both worlds” positioning. By that we mean that, despite having been somewhat late to enter the electric vehicle market, they have now proven their ability to produce competitive electric models, all the while continuing to build traditional internal combustion engine cars.

Although the transition to electric vehicles is in full swing and has been widely embraced by the industry, the pace of growth in demand for such cars across the Western world has been slowing down for some time now. “Early adopters”, customers with large means, have already made the shift. However, to “convert” the bulk of the population will require proposing smaller models, at affordable prices, as well as deploying a more extensive public charging infrastructure. We have clearly not yet reached that point.

Smaller cars are by definition limited in the size (and weight) of their batteries, hence in the distance they can travel between charges, causing some customer hesitancy to make the switch. A wait and see stance that seems all the more justified by the ongoing technological evolution, towards smaller batteries with higher and faster charging capacity. As regards prices, even assuming that the EU automobile industry does manage to bring them down to the targeted EUR 25,000 (from the current EUR 40,000 average), that will still substantially exceed the cost of a traditional car.

Chinese producers could of course undercut that price level, having developed models that they are now proposing in their national market for EUR 15,000-20,000. This massive Chinese push into electric vehicles is in fact partly responsible for the surge in iron ore imports, among others, that we highlighted last month. But while they do have the advantage of huge local demand (customers there being less hesitant to go electric), it seems unlikely that Chinese car makers will be allowed continued unhindered access to the EU and US markets.

2024 is an electoral year in Europe and imposition of some form of import taxes or restrictions on Chinese electric cars does seem in the cards. Germany is reluctant to take that route, probably because of the facilities owned by German manufacturers in China and also because it is the economy most vulnerable to retaliatory measures. But EU policymakers overall certainly do not want to see a repeat of what occurred in the solar panel industry – where EU producers have effectively been wiped out by Chinese competition.

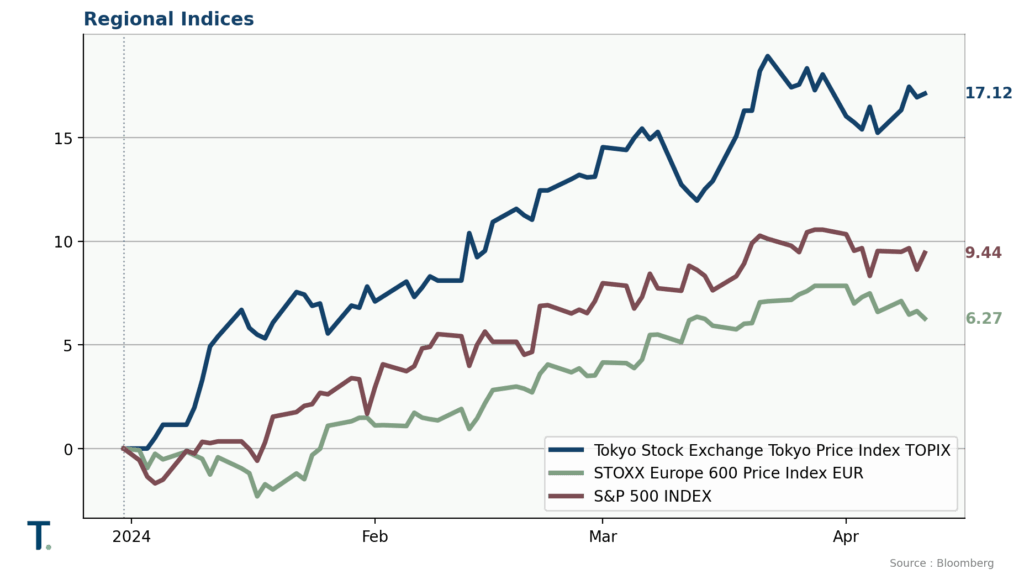

Also boasting an impressive performance over recent months have been Japanese equities. During the first quarter of 2024, the Topix index rose 17%, on top of a 25% gain in 2023.

Why such a rally? Although the Bank of Japan (BoJ) recently trimmed back its ultra-expansionary monetary policy, doing away with negative interest rate territory and putting an end to some unorthodox measures such as equity ETF buying, its stance remains quite “accommodative” by global standards. The fact that the yen currently sits at all-time lows against the US dollar should thus come as no surprise, and such a currency advantage is crucial for an open, export-driven, economy like Japan. Export growth has indeed accelerated, reaching an annual rate of 12% in January. An improving trend that is corroborated by other industrial indicators, such as the manufacturing PMI index.

In terms of valuation, the Topix index is currently trading at 16x forward expected earnings, in line with the 10-year average and similar to other major markets. This is thus no longer a bargain, and could eventually come under pressure if the BoJ continues to tighten policy. A scenario that is by no means impossible, given domestic inflation momentum and improving consumer confidence. At the same time though, we see few cheaper equity alternatives in Asia, beyond China where political intervention risk makes us reluctant to add exposure (despite the now clearly improving macro outlook).

All told, our message remains “more of the same”. Equity markets seem poised to continue their upward trajectory for a while, ahead of rate cuts later this year in both the US and Europe. The ride has probably not yet run its full course, but trees never grow to the sky either. Negative geopolitical developments and overly steep valuations due to excessive optimism are the dangers currently lurking around the corner. Some protection against these risks via (currently) cheap put options certainly cannot hurt.