Predicting how the conflict in Ukraine will evolve over the next days, weeks or months is near impossible – and the subject of widespread media coverage. We attempt here rather to reflect on its potential, and numerous, economic ramifications. For it is not just oil prices that stand to be impacted, but inflation in a much broader sense, as well global trade, GDP growth, corporate earnings… Not to forget central bank policy and public finances.

Tragically, one of the three hopes expressed in last month’s Investment Letter did not come true. Instead of reaching a form of truce regarding the separative Eastern provinces of Ukraine, Russian authorities chose to launch a full-fledged war. Within a matter of days, the situation has evolved to a point where the chances of a short-term “resolution” appear very low. Rather, it seems likely that the conflict will be a protracted one, with huge political, economic and, of course, human consequences.

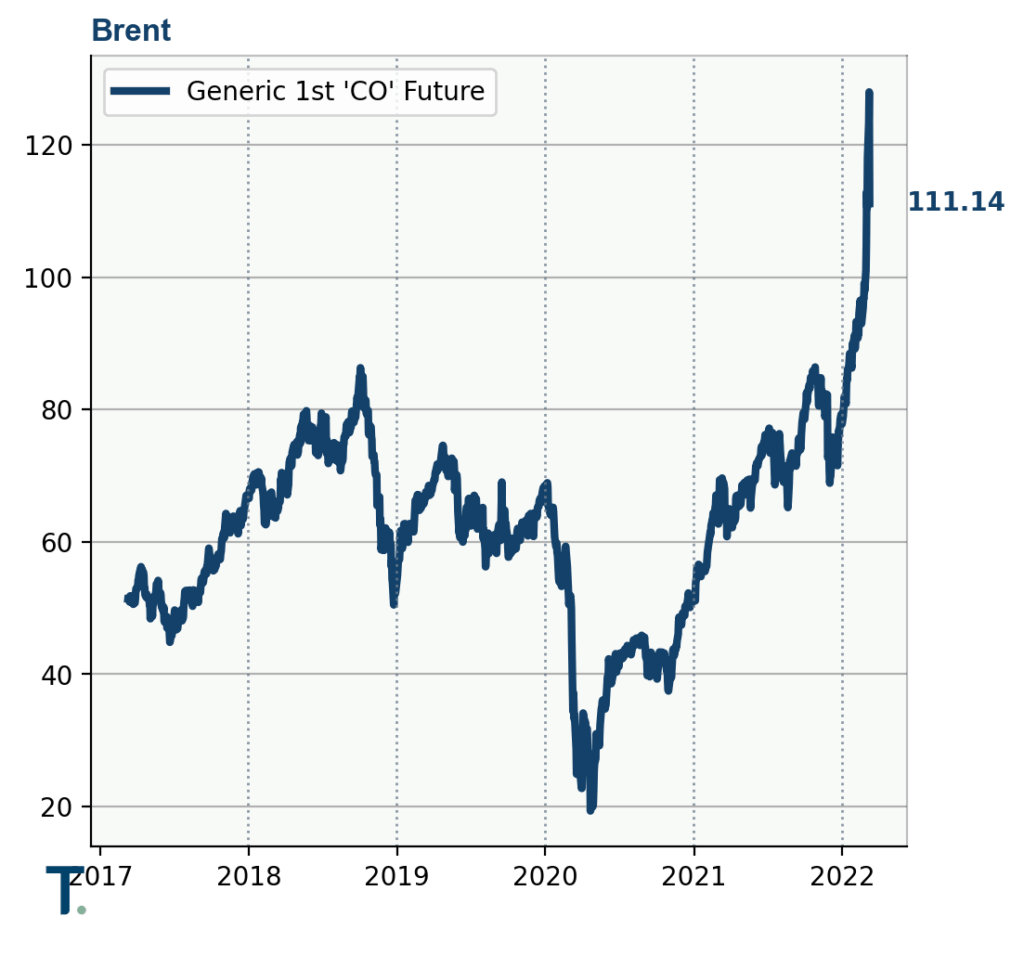

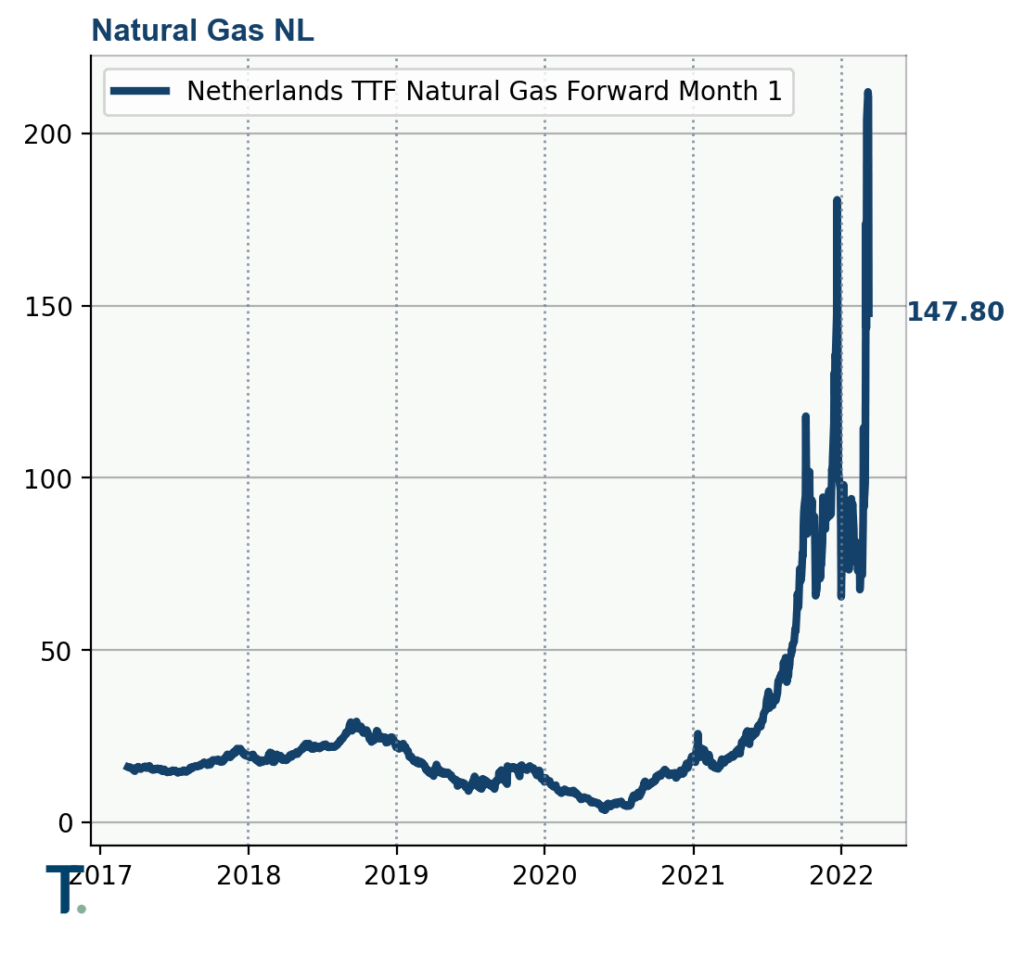

In economic terms, the first implication is that inflation is not about to go away. Indeed, the factors that have been pushing up prices for the past months, namely rising energy prices and supply chain disruptions, will only be made worse by the war that is now raging in Ukraine.

While we do not expect Russia to totally cut Europe off from energy deliveries, given that it will be needing the access to foreign currencies and reserves, the question is whether Europe will want to continue buying Russian output. Near-term, with 30-40% of gas consumed in Europe currently sourced from Russia (and even more in some countries like Germany), the answer is probably yes. But over the longer run, that may well change. Germany recently announced that it will build two new liquid natural gas terminals (to receive ships from Qatar and/or the US) and indicated, as has France, that – if necessary – it will be putting some coal-fired power stations back into activity.

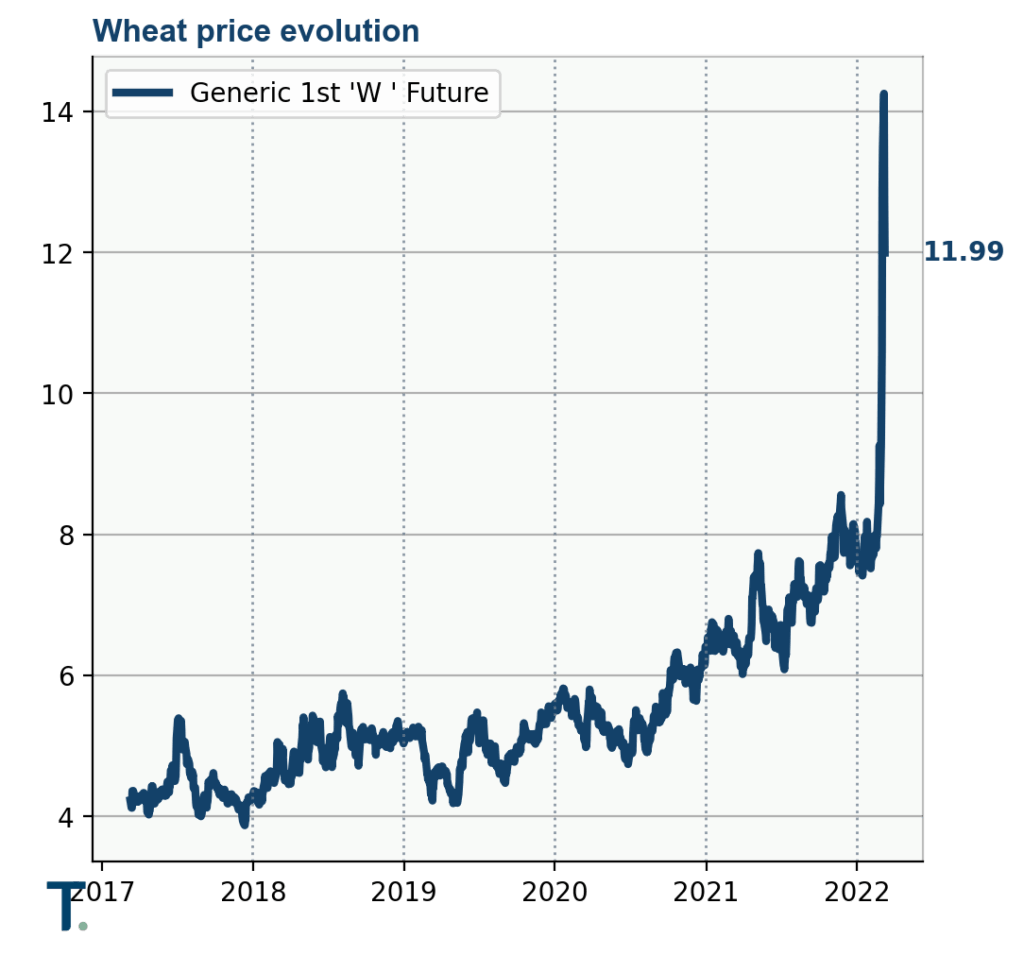

For consumers across Europe, one thing is clear: utility bills are moving up – and fast. In some countries they have already doubled, leading consumer organisations to push for price controls like those recently decided by the French government. In fact, nationalisation is no longer a completely unthinkable option! And energy prices are not the only issue, nor are the pressures limited to Europe. Just consider: Russia and Ukraine together account for a quarter of global grains trade, a share larger than that of the US and double that of the EU. Some emerging countries simply depend on the Russia/Ukraine breadbasket…

Shortly before the war began, the Federal Reserve (and even the European Central Bank) had finally admitted that inflationary pressures were not just a transitory, Covid-related, phenomenon. As such, bond markets had begun to price in a reduction in central bank balance bond purchases and even some policy rate hikes. With the new crisis, much of this move has been reversed. Expectations are again that central banks will not fight inflationary pressures, choosing rather to facilitate more debt build-up. This to finance the re-arming of Europe, further energy (and other price) subsidies, the inevitable strain on social systems due to massive influx of Ukrainian refugees and, still ever so necessary, the “green” energy transition.

From a trade perspective, this conflict has no less than the potential to take the world back to the pre-1989 era. A divided world, in which flows between the East and the West are pretty much halted. This too will weigh on corporate and economic growth going forward. Analysts have already halved their projection of 2022 European GDP growth, to around 2%, with the actual outcome liable to be worse even in our humble opinion.

Where does all this leave us as investors? Thus far, equity markets have not reacted that strongly, considering the gravity of the geopolitical developments. The TINA (“there is no alternative”) mantra appears to still have legs. That said, with valuations at lofty levels in historical terms and given the high odds that the conflict will endure, a serious correction cannot be excluded. And while our rather defensive strategy (underweight equity position and put options), combined with exposure to investment themes that have performed very well (energy in particular), is helping us navigate these stormier seas, we feel that some rebalancing of regional equity exposure is now also warranted. Reducing European exposure, where economic uncertainty and inflationary pressures are the greatest, and shifting this to the US and Japanese markets makes good sense today in our view.