What if President Trump’s unpredictability were actually part of a deliberate strategy to create chaos? With the end goal of securing the financial, economic and industrial dominance of the US, and having other countries foot the bill. So far, the only obstacles to these chaotic and sometimes illegal policies have come from US courts – including an important recent ruling on the tariff front – and negative financial market reactions (rising long-term interest rates and dollar depreciation).

The first few months of the Trump administration have been a roller-coaster ride, but with one manifest intention: bullying other nations to increase their spending on US products and services. Information technology (data processing, artificial intelligence, cloud computing) and the defence industry seem to be areas of particular focus. The presence of all major US technology CEOs at the January 20 inauguration ceremony can be seen as a sign of pure opportunism. And the pressure exerted by the US defence secretary, during his recent trip to Asia, on Far Eastern allies to hike their defence budgets to 5% of GDP was not just a matter of them gearing up for immediate geopolitical risks (a Chinese invasion of Taiwan?). It is also a means of boosting future revenues for US manufacturers of military equipment.

Cashflows from abroad the US are indeed necessary to fulfil two of President Trump’s key campaign promises: boosting domestic employment and cutting taxes for US corporations and citizens, as provided for in the ”One, Big, Beautiful Bill Act” (Trump speak) currently being debated by the US Congress. This represents the Trump administration’s budget proposal for the coming years, but it involves a very large deficit. Revenues from import tariffs would, of course, help finance the “One Big Beautiful Bill Act” (OBBBA), but the US Court of International Trade recently ruled that resorting to the “International Emergency Economic Powers Act” in order to impose across-the-board tariffs is not legal. Although the White House has filed an appeal, odds are that higher courts will uphold this decision.

A more targeted approach to import tariffs is thus likely to be adopted by the Trump administration, placing greater emphasis on specific nations and/or industries. An obscure section (899) of the OBBBA is also starting to arouse concern within the international financial community. It aims to increase tax rates for individuals and corporations based in countries judged to have “discriminatory tax policies”. Put differently, it creates the possibility of imposing additional taxes on foreign investors in US stocks and bonds, on their future dividend and interest revenue.

The underperformance of US government bonds certainly has something to do with this. They already reflect lesser demand by international investors – if not outright dumping by China. Indeed, for the US’s greatest adversary, reducing the amount of US Treasuries held by its central bank serves both as a weapon in the ongoing trade war and a protection against a potential freeze on capital flows (such as Russia experienced first-hand a few years ago).

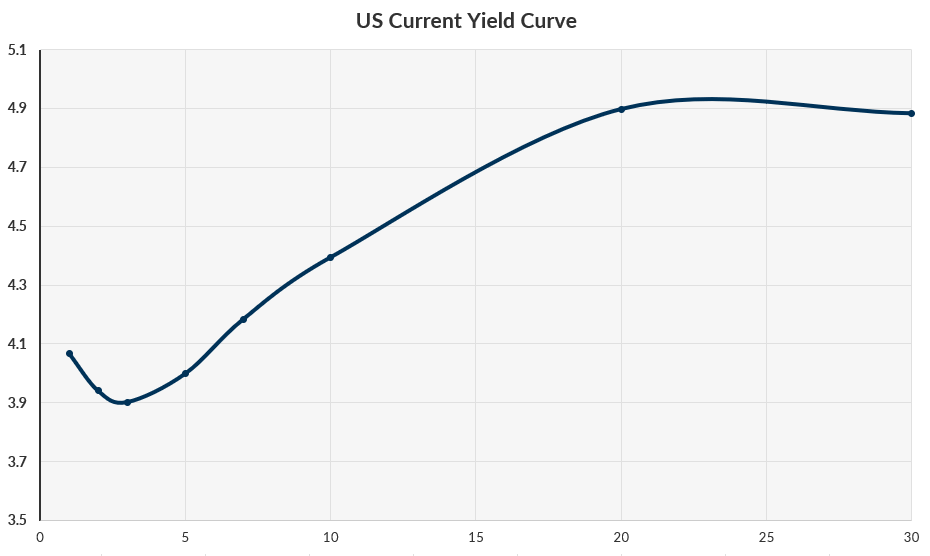

Speaking of the US government bond market, we should also point out the highly unusual shape of the yield curve (see graph). It is positively sloped up to a 3-month term, inverted for maturities of three months to 3 years, positive again through to a 20-year term, and fairly flat between 20 and 30 years. The market thus expects the Fed to cut rates in the relatively near future, but finds the longer term outlook rather worrisome. Either because of the risk of inflation getting out of hand, or because of US public debt reaching unsustainable levels (the “term premium”).

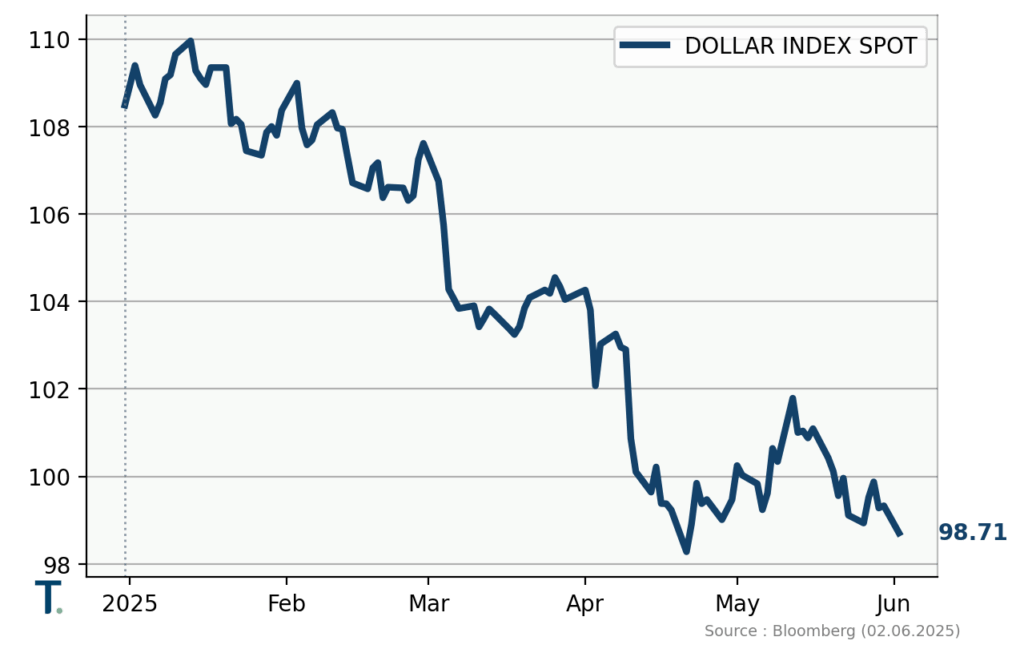

Recent US dollar depreciation, against virtually all major currencies (see chart), also reflects such concerns regarding the US economic and debt trajectories. We see little reason for this pattern to reverse course, hence confirm the “underweight” exposure to the greenback in our investment portfolios.

What then of equity markets, which appear to be painting a much more optimistic picture (even though US indices are lagging their international peers year-to-date)? The fact that early year losses have been largely recouped, and that most markets are trading close to historical highs, has more to do, we would argue, with excess liquidity in the system (resulting from prolonged money printing by central banks after the Great Financial Crisis and during the Covid pandemic) than with real economy trends. First quarter corporate earnings were admittedly solid, but there are mounting signs of business leaders lowering future guidance and/or being reluctant to make investments, because of policy unpredictability (especially in the US).

Also certainly a factor in buoyant equity market performance is the growing involvement of (young) private investors (so-called “hammock investors”). Fuelled by social media posts by “finfluencers” on how to make “easy money” on the stock market, they are buying equity ETFs (index trackers) in large numbers, pushing all stocks upward. With everything rallying, it is understandable that they no longer bother to perform a thorough analysis of company fundamentals and valuation (assuming they were capable of doing so in the first place).

Only when a serious and prolonged correction occurs will the wheat finally be separated from the chaff – and real bargains to be had.

In the meantime, and in light of the geopolitical chaos, we believe that a broadly diversified portfolio remains the most appropriate means of preserving capital.

Header Image Credit : Kevin Dietsch/Getty Images